Pursuing higher education abroad is a dream for thousands of Indian students every year. However, the financial requirement, which often runs into lakhs or even crores of rupees can be a major barrier. Education loans for overseas studies help bridge this gap, but choosing the right education loan provider is critical. A poor choice can burden you with high costs, rigid terms, and repayment stress.

In this complete guide, you will learn how to choose the best education loan provider in India for overseas education, understand what to evaluate, compare key lenders, and make a confident decision.

Why Choosing the Right Education Loan Provider Matters

The choice of provider affects:

- Cost of borrowing through interest rates

- Speed of disbursement, affecting university deadlines

- Flexibility of repayment and moratorium benefits

- Documentation and ease of processing

- Tax benefits under Indian law

A small difference in interest rate or processing fees can translate into lakhs of rupees over the loan tenure. That’s why this decision should be deliberate, not rushed.

What Makes Overseas Education Loans Different?

Education loans for study abroad cover a wider range of needs, including:

- Tuition fees

- Living expenses

- Travel (airfare)

- Exam & library fees

- Laptop and other equipment

- Insurance and miscellaneous costs

Because the amounts are larger and risks perceived higher, lenders often require stricter documentation and sometimes collateral security.

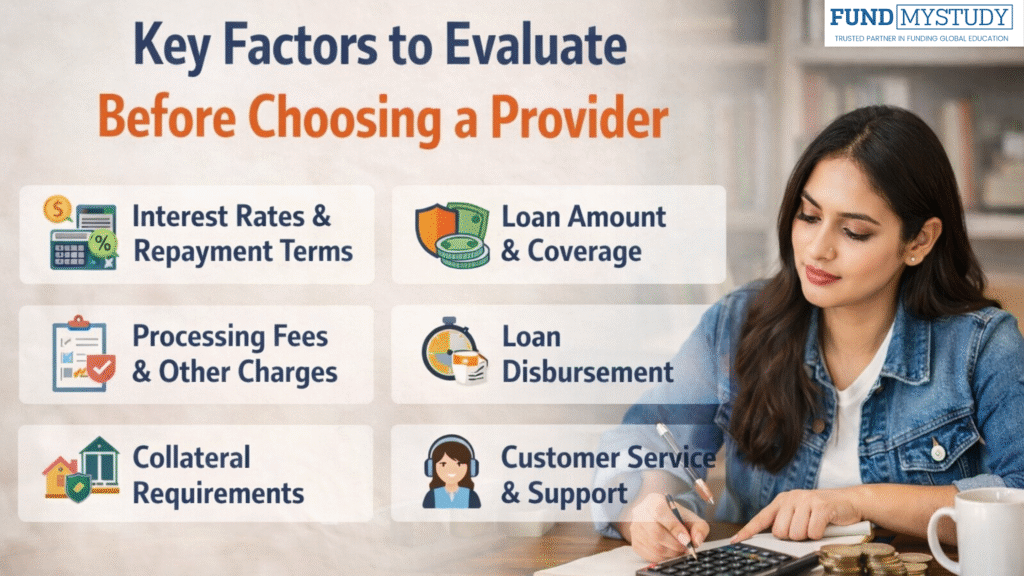

Key Factors to Evaluate Before Choosing a Provider

Below are the most important criteria to compare when selecting an education loan provider:

- Interest Rates

- Processing Time

- Collateral Requirement

- Loan Tenure & Moratorium Period

- Repayment Benefits & Flexibility

- Co-applicant Criteria

- Customer Support & Digital Experience

Overview Table: Key Loan Provider Features

| Feature / Provider | Public Banks (e.g., SBI, PNB) | Private Banks (HDFC, ICICI) | NBFCs (Avanse, Credila) | Government Schemes |

| Interest Rate | Lower | Moderate | Moderate–High | Subsidized |

| Processing Time | Medium (10–30 days) | Medium (10–25 days) | Fast (5–15 days) | Depends on bank |

| Collateral | Yes (above limits) | Yes/Partial | Often No | As required by bank |

| Loan Amount | Up to course cost + extras | Up to course cost + extras | Up to full cost | Available |

| Moratorium | Course + 6 months | Course + 6 months | Course + 6 months | Course + 6 months |

| Flexibility | Standard | Better | High | Governed by bank |

1. Interest Rates — Compare Carefully

Interest rates determine your overall cost of borrowing. Even a 1% difference can add up substantially over an 8–15 year tenure.

- Public sector banks usually provide the lowest eligible interest rates due to government support.

- Private banks tend to have slightly higher interest but better customer service and digital processes.

- NBFC student loan providers specialize in overseas education and may offer loan without collateral, but often at a higher rate.

You can also read our comparison on education loan providers in India including overseas options

2. Loan Processing Time — Why It Matters

Processing time determines whether your loan will be disbursed before your university’s payment deadline. Typical processing timelines:

- Public Banks: 10–30 days

- Private Banks: 10–25 days

- NBFCs: 5–15 days

If your university has strict fee deadlines, choosing a lender with faster processing or good support for quick documentation helps avoid late penalties.

3. Collateral vs Non-Collateral Loans

Collateral requirement is a major deciding factor:

- Collateral: Asset or security (like fixed deposits, property) that backs the loan.

- Non-Collateral: No asset required, but may have higher interest.

For overseas education, many NBFCs and private lenders offer non-collateral loans up to a certain limit, reducing the documentation burden.

4. Loan Tenure & Moratorium Period

- Loan Tenure: Maximum time you have to repay the loan — usually 10–15 years for overseas education loans.

- Moratorium Period: This is interest-only or no-repayment time until after course completion — usually course duration + 6 months.

Longer tenure and flexible moratorium help reduce monthly EMIs initially and make repayment manageable once you start your career abroad.

5. Repayment Flexibility & Benefits

Good lenders offer:

- Step-up EMIs (lower initially, higher later)

- Top-up loans for ancillary expenses

- Prepayment without penalty

- Part-repayment benefits

Understanding these subtle differences helps maximize your financial comfort.

6. Co-Applicant and Eligibility Requirements

Most lenders require a co-applicant, often a parent, spouse, or guardian. Their

- Credit score

- Income stability

- Existing loans

can affect approval chances and interest rates. Choose a co-applicant with strong financials and clear credit history.

7. Support and Digital Experience

When studying abroad, you may need quick access to loan status, document uploads, or support. Providers with mobile apps, online tracking, and responsive support make the experience smoother.

Comparing Providers: What Works Best for You?

Here’s how common providers stack up for study abroad loans:

Public Sector Banks

- Best for: Lower interest and strict rules

- Good fit: Government-linked initiatives, long-term planning

Private Banks

- Best for: Modern digital support, flexible repayment

- Good fit: Students who prefer tech-friendly experience

NBFCs (e.g., Avanse, Credila)

- Best for: Quick processing, non-collateral loans

- Good fit: Students with tight timelines

Government Education Loan Schemes

- Best for: Interest subsidies and tax support

- Good fit: Students eligible under government criteria

Checklist Before You Finalize a Loan Provider

✔ Understand the full cost of borrowing (interest & processing fees)

✔ Check loan disbursement timelines

✔ Confirm collateral requirements

✔ Verify moratorium period and repayment flexibility

✔ Ask about prepayment charges

✔ Review customer support quality

FAQs — Education Loan for Overseas Studies in India

1. What is the ideal interest rate for an overseas education loan?

There is no fixed “ideal,” but lower rates (closer to public bank rates) reduce overall cost. Compare between 9% and 13% as a general range based on current banking trends.

2. Can I get a student loan without collateral for overseas studies?

Yes — many NBFCs and private banks provide non-collateral loans up to certain limits depending on credit profile and co-applicant strength.

3. How long does it take to process an overseas education loan?

Typical timelines range from 5 to 30 days based on lender type and document completeness.

4. What expenses does the loan cover?

Many loans cover tuition, living expenses, travel, laptop, insurance, and other academic fees.

5. Are there tax benefits on education loans?

Yes — interest paid on education loans qualifies for deduction under Section 80E of the Income Tax Act. (You may link to official tax guidance like https://www.incometaxindia.gov.in for details.)